Alaska Coastal Oil Drilling Challenge Revived by U.S. Court

Alaskan coastal drilling by oil companies including ConocoPhillips (COP:US) and Royal Dutch Shell Plc (RDSA) may be further delayed after a U.S. court revived conservation group claims that the government acted illegally in opening almost 30 million acres on the continental shelf to energy exploration.

Alaskan coastal drilling by oil companies including ConocoPhillips (COP:US) and Royal Dutch Shell Plc (RDSA) may be further delayed after a U.S. court revived conservation group claims that the government acted illegally in opening almost 30 million acres on the continental shelf to energy exploration.

By Karen Gullo January 22, 2014

Alaskan coastal drilling by oil companies including ConocoPhillips (COP:US) and Royal Dutch Shell Plc (RDSA) may be further delayed after a U.S. court revived conservation group claims that the government acted illegally in opening almost 30 million acres on the continental shelf to energy exploration.

Sierra Club and other organizations sued the government after the $2.6 billion sale of development leases for the Chukchi Sea off the northwest coast of Alaska in 2008, saying the amount of oil from the leases was far higher than the 1 billion barrels the U.S. Interior Department had estimated in an an environmental review.

The U.S. Court of Appeals in San Francisco today concluded the estimate was “chosen arbitrarily” and meant that the Interior Department “based its decision on inadequate information about the amount of oil to be produced pursuant to the lease sale.” The decision reverses a judge’s 2012 ruling dismissing the lawsuit.

“The agency is going to have to revise or supplement its analysis of the lease sale,” Erik Grafe, an Earthjustice attorney who argued the case, said in a phone interview. “We think the agency shouldn’t allow any drilling on this basis.”

Marjorie Weisskohl, a spokeswoman for the Interior Department, and Kelly op de Weegh, a spokeswoman for The Hague-based Shell, didn’t immediately respond to voice-mail messages seeking comment on the ruling.

Bush Administration

The conservation groups said in their complaint that the Bush administration’s decision to open the Chukchi Sea to oil and gas exploration violated the U.S. National Environmental Policy Act.

The U.S., saying that the Bureau of Ocean Energy Management already had analyzed the environmental impact at the behest of a federal judge in Alaska, contended that supplemental environmental impact statements had adequately addressed the impact of drilling on whales and other species as well as the generation of greenhouse gases.

ConocoPhillips, based in Houston, and Shell’s Gulf of Mexico unit joined the case on the side of the federal government.

The case is Native Village of Point Hope v. Jewell, 12-35287, U.S. Court of Appeals for Ninth Circuit (San Francisco).

To contact the reporter on this story: Karen Gullo in federal court in San Francisco at kgullo@bloomberg.net

To contact the editor responsible for this story: Michael Hytha at mhytha@bloomberg.net

Shell working to contain fire at Texas facility

Source: Reuters – Wed, 22 Jan 2014 09:19 PM

Jan 22 (Reuters) – Royal Dutch Shell Plc emergency personnel were trying to contain a fire at its facility in Deer park, Texas, the oil company said in a message posted on a community information phone line on Wednesday.

The Deer Park facility houses a 327,000 barrel-per-day (bpd) refinery and a chemical plant and is a 50-50 joint venture between Shell and Mexican national oil company Pemex.

The fire will not affect the community, industrial neighbors or other operating units at the facility, the message from an environmental supervisor at the plant said.

Big Oil Is Unloading Billions of Assets in Spring Cleanup

Royal Dutch Shell PLC decided it’s time to clean out its global energy portfolio. The oil giant could unload as much as $30 billion in assets as part of the purge.

by Matt DiLallo, The Motley Fool Jan 22nd 2014

Royal Dutch Shell PLC decided it’s time to clean out its global energy portfolio. The oil giant could unload as much as $30 billion in assets as part of the purge.

Shell gameShell needs to make some changes after it warned that its profits would be significantly lower than analysts were expecting. But the company has been hinting for a while that it would be paring back its portfolio. Earlier this year Shell announced it was exiting several U.S. shale basins after returns failed to meet its expectations.

Because of this the company is looking for buyers for itsMississippian Lime assets in Kansas and Oklahoma as well as itsEagle Ford Shale assets in Texas.

Shell’s Recent Profit Warning Won’t Be the Last

Thanks to upstream cost overruns and downstream overcapacity, 2013 probably will not be the last year Shell faces low earnings. Not only is Gorgon facing big challenges, the Shell-ExxonMobil-Total-KazMunaiGas-Eni Kashagan project was recently shut down due to pipeline leaks. The field’s current $50 billion cost is more than five times its original price

Thanks to upstream cost overruns and downstream overcapacity, 2013 probably will not be the last year Shell faces low earnings. Not only is Gorgon facing big challenges, the Shell-ExxonMobil-Total-KazMunaiGas-Eni Kashagan project was recently shut down due to pipeline leaks. The field’s current $50 billion cost is more than five times its original price

By Joshua Bondy: January 22, 2014

Royal Dutch Shell (NYSE: RDS-A ) just issued a big profit warning for the fourth quarter of 2013, bringing its expected full-year 2013 earnings to $16.8 billion. This is a significant fall from its 2012 full-year earnings of $27.2 billion. Thanks to upstream cost overruns and downstream overcapacity, 2013 probably will not be the last year Shell faces low earnings.

Downstream challengesShell’s refineries put a hole in its Q4 2013 earnings. Its Asia-Pacific and European refineries are facing margin pressures and for good reason. They don’t have access to cheap U.S. crude. They are forced to buy expensive Brent crude and pay a premium relative to U.S. refiners. Also, U.S. refiners have access to cheap natural gas and natural gas liquids.

As of Dec. 31, 2012, Shell had equity interests of at least 13% in eight Asian refineries. As if feedstock issues weren’t enough, the Asian refinery market is facing overcapacity and low margins for years to come. Thanks to expansions in India, China, and other nations, analysts project that Asia could have a refining surplus of up to 3 million barrels per day in 2018.

HollyFrontier (NYSE: HFC ) is the opposite of Shell. HollyFrontier operates five small refineries with a total capacity of 443,000 barrels per day of capacity. Thanks to its location in the American Midwest it has great access to cheap crudes, with a number of promising investments on the table. For $300 million HollyFrontier is expanding its Woods Cross facility to produce a relatively secure $125 million in additional annual earnings before interest, taxes, depreciation, and amortization.

HollyFrontier does have its challenges. The closing Brent-West Texas Intermediate spread will put downward pressure on its net income. HollyFrontier’s 2012 net income per barrel was more than $10, but it could head toward the $2.69 average it posted from 2001 to 2010 when WTI traded at a premium to Brent.

Shell’s upstream challengesThe huge Gorgon LNG project keeps seeing cost increases. Recently the big partner, Chevron (NYSE: CVX ) , upped the project’s cost by $2 billion to a total of $54 billion. This cost increase comes after Chevron previously added $15 billion to Gorgon’s price tag. Cost overruns are hurting Big Oil across the board, as Shell andExxonMobil (NYSE: XOM ) each own 25% of Gorgon.

Not only is Gorgon facing big challenges, the Shell-ExxonMobil-Total-KazMunaiGas-Eni Kashagan project was recently shut down due to pipeline leaks. The field’s current $50 billion cost is more than five times its original price, and recent delays have pushed back its commercial start date even further. High levels of hydrogen sulfide make production especially difficult and point to further setbacks in the years to come.

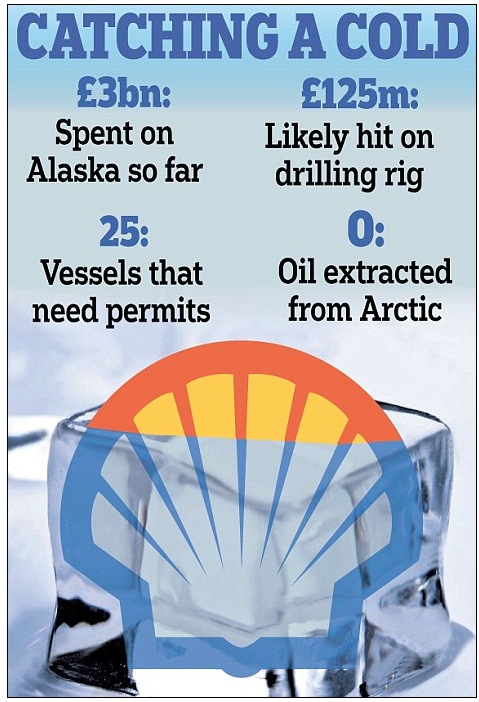

In addition to the aforementioned problem projects, Shell’s expensive Arctic drilling has come up short.

Delays and cost overruns in these big projects mean more of Shell’s cash must be diverted toward capital expenditures. At the same time there is less money flowing in from production. From 2012 to 2013 Shell’s net capital investment is expected to increase from $29.8 billion to $44.3 billion. Lower upstream volumes are another negative factor for Shell, helping to push expected Q4 2013 upstream earnings down to $2.5 billion from $4.4 billion in Q4 2012.

Once more of Shell’s big upstream projects come online, its volumes and earnings should head upward; but it may be a number of years or more until the major kinks are worked out.

Shell is not aloneCost overruns and upstream production challenges are not unique to Shell. In the last four quarters, ExxonMobil saw its revenue fall from $126 billion to $109 billion and its EBITDA fall from $33 billion to $15 billion. Its presence in both the Gorgon and Kashagan projects has put stress on ExxonMobil’s capex budget.

Just as Shell is having problems trying to maintain its upstream volumes, ExxonMobil is facing similar challenges. ExxonMobil was able to boost its Q3 2013 upstream volumes relative to Q3 2012 but only by 1.5% on an oil-equivalent basis. In Q3 2013 it produced a massive 4 million barrels of oil equivalent per day, and there is a good chance this could fall slightly in the coming years. There are only so many mega-projects available in the world.

Chevron is a different storyChevron will have an easier time maintaining its upstream volumes than ExxonMobil. In Q3 2013 it produced 2.6 million barrels of oil equivalent per day, significantly less than ExxonMobil’s 4 mmboepd. Chevron is active in the Vaca Muerta region in Argentina, off the coast of the Congo, and it is already producing in the Brazilian Papa-Terra field.

In the last four quarters Chevron’s EBITDA did fall from $14 billion to $11 billion, but compared to ExxonMobil it fared much better. Overall Chevron’s smaller size will help it to be more nimble and stay out of projects like Kashagan.

Final thoughtsShell is a massive company stuck with many refineries and expensive greenfield projects. It has a challenging future ahead as it struggles to bring large upstream projects online and on budget. Investing in smaller companies like HollyFrontier or Chevron helps you make sure that your investment dollars are shoved into fewer $50 billion dollar quagmires.

Shell CEO plays ‘new boss’ card

Royal Dutch Shell’s chief executive Ben van Beurden has, on the face of it, played the classic “new boss” card – using a barely justified profit warning to brighten his own future by making the past look bad. The truth is quite different, the energy company says, and possibly far more worrying for investors. ”After taking legal advice we concluded we had an obligation to disclose the Q4 numbers as soon as possible in order to comply with stock exchange rules on fair disclosure.”

ANDREW CALLUS: 22 Jan 2014

Royal Dutch Shell’s chief executive Ben van Beurden has, on the face of it, played the classic “new boss” card – using a barely justified profit warning to brighten his own future by making the past look bad.

The truth is quite different, the energy company says, and possibly far more worrying for investors.

Three trading days after van Beurden’s warning last Friday that quarterly net profit will fall far short of expectations, Shell’s shares are barely down 1.5 per cent in a flat market.

But while circumstances conspired to make the fourth quarter particularly bad for Shell, there is no guarantee that the group will bounce back this year.

Van Beurden, some shareholders say, must do more than tighten up a bit and sweep away a few cobwebs when he reveals his strategy in March.

A fortnight into his tenure, the Dutchman broke a traditional pre-results silence at Europe’s biggest investor-controlled oil company.

Pre-empting the official announcement on January 30, he revealed numbers showing October-December last year was Shell’s worst quarter since 2009.

He also called the whole 2013 performance “not what I expect from Shell”.

Few commentators and analysts failed to connect the rhetoric with the fact that removal boxes have scarcely been cleared from the boss’s office in The Hague.

Using such warnings, new chiefs frequently try with varying degrees of subtlety to shift the blame for a company’s problems on to the past leadership, and lower expectations for their own tenure.

“It’s standard practice, but this was done very transparently, and that’s high risk,” said a person who has deep experience of corporate presentation strategies, but was not involved.

“Everyone knows the game he is playing.”

At US$2.9 billion ($3.5 billion) for adjusted earnings on a current cost of supply basis, the fourth quarter net profit figure van Beurden gave was well below market expectations of around US$4.0b.

But misses like this are common in the energy industry, and rarely have a significant or long-lasting impact on investor sentiment. Profit warnings to flag them are also rare.

Shell missed forecasts just as badly in the second quarter last year, making a US$4.6b profit compared with analysts’ average prediction of US$5.7b.

That time it did not alert shareholders in advance. Neither did it when profits beat estimates by a similar amount in the first three months, making US$7.5b versus the US$6.5b forecast.

Some of Shell’s rivals have also produced surprises in the past two years, with results both above and below expectations.

Executives and investors alike insist that quarterly and even annual performance is a poor measure of an industry that works on much longer investment timescales.

Some also question the quality of forecasts made by analysts at brokerages and investment banks.

The rest of van Beurden’s statement went over old ground, citing “weak industry conditions in downstream oil products, higher exploration expenses, and lower upstream volumes”.

For the oil and gas production division – the main driver of profits – van Beurden said there had been a high level of maintenance activity during the quarter in high value production areas, including the Pearl Gas to Liquids (GTL) plant in Qatar, and in Liquefied Natural Gas (LNG).

Security in Nigeria continued to be “challenging”, he said, US operations remained lossmaking, and currency factors in Australia had worked against the company.

All of these factors had already been flagged by finance director Simon Henry at the end of October, in some detail.

“Our focus will be on improving Shell’s financial results, achieving better capital efficiency and on continuing to strengthen our operational performance and project delivery,” van Beurden promised, using words his predecessor, Peter Voser, would recognise.

DEEPER WORRY

So much for appearances. Shell had deeper concerns, according to Andy Norman, the company’s Vice President Media Relations.

His comments set against the limited market reaction suggest management is far more shocked than investors have been by the scale of the downturn.

Shell says the warning was dictated neither by analysts’ average or “consensus” forecast nor the new leadership.

“Consensus was not a factor in the announcement,” Norman told Reuters, adding: “These decisions are made by clear accounting rules. They’re not influenced by senior executive changes.”

Norman acknowledged that when Shell announced its third quarter results it flagged operational factors that were likely to make the rest of the year tough.

“While this operational guidance was correct, the factors turned more negative than we expected during the quarter,” he said.

“At US$2.9b, Q4 earnings are expected to be well below the US$5-7b range we’ve typically seen in most quarters in recent years.

“After taking legal advice we concluded we had an obligation to disclose the Q4 numbers as soon as possible in order to comply with stock exchange rules on fair disclosure.”

How much the fourth quarter problems persist is crucial, according to Oswald Clint, analyst at Bernstein.

“It may be that everything went against Shell this quarter but it doesn’t mean it will bounce back next quarter either,” he said.

Even before Friday’s statement, investors were increasingly expecting radical action from van Beurden, who was promoted to the post on January 1 after Voser’s surprise early retirement. He has his chance at a strategy day on March 13.

“The market’s not going to judge him on this (statement), but they will be disappointed if – come that first management strategy day where he stands up and gives his vision – it’s all a bit more of the same, a bit of tightening up and sweeping away a few old cobwebs,” said a British-based institutional shareholder who asked not to be named.

“That’s not going to be enough.”

Some analysts and investors advocate a gradual structural move towards high-margin LNG, and away from moribund refining – a departure from the traditional integrated oil model which they hope might highlight the value in Shell’s market-leading LNG position.

Others want to go in that direction more quickly. There has also been talk the underperforming US business may be jettisoned entirely.

BEURDEN OF RESPONSIBILITY

Leaving aside more radical measures, van Beurden’s task is tricky – not least because this week he lost his head of international upstream operations, Andy Brown, for an unspecified period of medical leave.

Van Beurden has little room for manoeuvre in an industry that has to invest 10 and 15 years ahead, yet must satisfy shareholders with a much shorter attention span.

“I’d be surprised if you were looking at radical changes because an awful lot of the project pipeline – stuff that takes years to put together – it’s not easy to move that around,” said VTB Capital analyst Colin Smith.

Shell’s net investment spending – money flowing out – was $44.3b in 2013. Cash flow from operations – money in – was US$40.4b.

Those two numbers broadly reflect level or falling output and prices set against rising costs, and they show that Shell effectively “burned” nearly US$4b last year.

Shareholders fear for their US$11b of annual dividends as a result, and Shell has been seen as the least attentive of its peer group to this industry-wide concern.

Returns on investment data going back to April 2010 show the company underperforming three out of four of its main rivals – the fourth being BP, which took a direct hit from the Gulf of Mexico oil spill in that month.

Lately though, like its peers, Shell has promised that capital spending has peaked. Its move to abandon a GTL project in the United States and likely abandonment of its Arrow LNG project in Australia are signs of those efforts.

Also falling into line with its rivals, Shell has promised to step up asset sales, an action which both brings in cash and cuts outgoings.

Shell has a four-year net investment target of US$130b for 2012 to 2015.

Including US$30 billion spent in 2012 and US$44.3b in 2013, it spent over US$74b in the first two years.

That leaves less than US$23b a year for 2014 and 2015, US$20b short of 2013′s budget.

If van Beurden is going to meet that target – and some say he will dump it either on January 30 at the results day or at the March strategy day – he will have to make up that gap through US$20b a year-worth of asset sales, project-abandonment, and other cost saving measures.

– Reuters

The TRUTH will set you FREE.

No comments:

Post a Comment