Potentially, a prolonged period of low oil prices might finally see BP and Shell, like two drunken sailors, holding each other up through the merger that has so long been on the horizon.

Potentially, a prolonged period of low oil prices might finally see BP and Shell, like two drunken sailors, holding each other up through the merger that has so long been on the horizon.

“ALEX BRUMMER: Big oil players confront the slump by slashing capital expenditure”

Oil exploration and production is a long-term enterprise so it is encouraging that Shell chief executive Ben van Beurden is not hitting the panic button.

The group’s market value of £139billion makes it the biggest beast on the FTSE 100 by a long chalk. In that context, and with its strong cash flows, the asset disposals and the proposed cuts in capital spending of $15billion (£9.9billion) over three years are relatively modest.

In pressing on with capital expenditure, despite the fall in the oil price by 60 per cent over the last year, Shell looks to be counting on energy prices bouncing back. It is an interesting assumption because there is a prevailing view that there has been a mispricing of oil for a lengthy time because of a glut of supplies.

It is fairly remarkable that despite the worsening conflict between Russia and Ukraine, allied bombing raids on Islamic State in Northern Iraq and chaos in Libya there is still plenty of oil to go around. The financial speculation that has driven prices higher has been removed from the market.

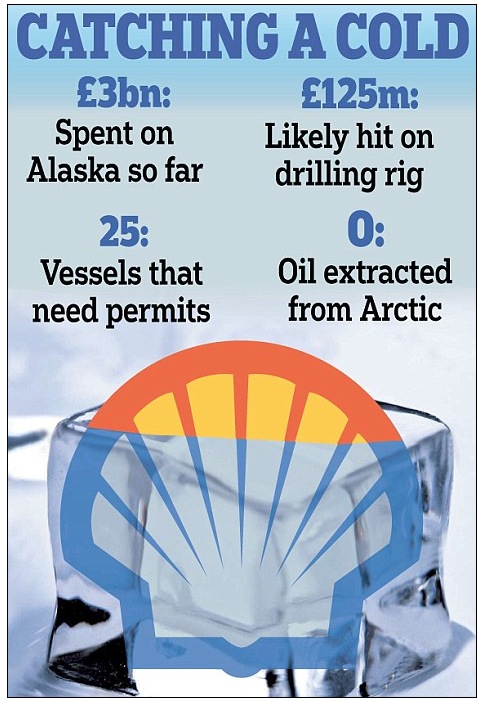

What is perhaps most surprising is Shell’s determination to press ahead with Arctic drilling despite all the flak it has taken from green activists and North American environmental enforcers.

Van Beurden recognises that Arctic exploration is not easy and calmly notes it ‘divides society’ but is keeping the option open.

The company has spent some $1billion on preparing its drilling in Alaska’s Chukchi Sea and is spending several hundred million dollars keeping the prospect alive despite the huge obstacles.

The determination with which it is approaching something so difficult and costly, when market prices are at a low ebb, suggests that it regards the Arctic as one of the world’s great unexploited energy assets. It is much the same thinking that led Bob Dudley to get into bed with the Russian national oil firm Rosneft, in the belief BP would have the first crack of extracting oil from the Russian Arctic.

The market clearly wasn’t too impressed with Shell’s final quarter results. But it can hardly be surprised that earnings came in below forecasts.

The bigger concern might be that it is over-optimistic on future oil prices and it may have to retrench in 2015 potentially placing dividend payments that totalled $12.2billion last year in jeopardy.

Shell, no doubt, also is keeping close tabs on what its beaten-up rival BP is up to. Over the decades the two London quoted oil giants have gingerly circled each other looking for a moment to pounce with a takeover offer. Shell is without doubt in a far better place now despite persisting problems in Nigeria.

But they are as nothing compared with the $43billion of disposals that BP has had to make to feed the compensation claims, fines and other penalties over the Deepwater Horizon oil spill of 2010.

BP’s latest disposal of stakes in two large Gulf of Mexico oilfields to American rival Chevron (also a potential merger partner) suggests that after decades of investment in the United States, including the takeovers of Arco, Amoco and Sohio, BP is now less than enamoured with the United States.

Potentially, a prolonged period of low oil prices might finally see BP and Shell, like two drunken sailors, holding each other up through the merger that has so long been on the horizon.

RELATED

Shell cuts capital spend by $15bn in ‘significant message’ that oil industry is changing but maintains profit and dividend

Royal Dutch Shell is the latest oil company to announce cost-cutting measures to combat the plunging price of crude despite unveiling a 12 per cent rise in fourth quarter underlying profit.

The blue chip heavyweight is to cut £15billion (£9.9billion) from its spending plans over the next three years joining peers in belt-tightening as it responds to a change in market conditions which has seen Brent crude prices more than half since last summer.

Shell said it has decided that a number of capital projects previously planned won’t now go ahead because they are commercially unfeasible at the current level of oil prices.

But the Anglo-Dutch giant pledged not to over-react to the decline in oil and said lower prices created opportunities to reduce its own costs.

The comments came as Shell posted a 12 per cent rise in underlying profits to £2.15billion for the final quarter of 2014, although that was below City expectations.

The Q4 performance was boosted by recent efforts to restructure its downstream operation, as well as increased output of higher-margin products.

However, profits for its upstream exploration and production division still fell by 30 per cent to £1.14billion in the quarter.Prudent: CEO Ben van Beurden said ‘Shell is taking structured decisions to balance growth and returns.’

Chief executive Ben van Beurden said: ‘We are taking a prudent approach here and we must be careful not to over-react to the recent fall in oil prices.

‘Shell is taking structured decisions to balance growth and returns.’

The spending cut, which will involve cancelling and deferring projects, represents a 14 per cent reduction from its 2014 capital investment of $35billion and reverses the group’s announcement in October that it would keep 2015 spending unchanged.

‘Shell is considering further reductions to capital spending should the evolving market outlook warrant that step, but is aiming to retain growth potential for the medium term,’ it said in a statement.

At lunchtime, Royal Dutch Shell’s shares were more than 4 per cent lower, off 90.0p at 2,063.5p.

However, in a move designed to placate investors, Shell is keeping its level of dividends unchanged.

Shell maintained its fourth quarter payout at $0.47 per share and in a rare move pledged to pay the same amount in the first quarter of 2015.

Keith Bowman, equity analyst at Hargreaves Lansdown Stockbrokers said this was a key reason why he still recommends Shell shares as a buy.

Bowman said: ‘Management is underlining its determination to respond to the falling oil price, with cuts to capital spending being announced.

‘As expected, fourth quarter performance has been impacted by the lower oil price, although downstream refining operations have provided some counterbalance.

‘In all, and despite the disappointing numbers, the dividend payment remains core, with the payment being left unchanged. For now, and given the attractive dividend yield in the current low interest rate environment, analyst consensus opinion points towards a buy.’

Graham Spooner, investment research analyst at The Share Centre said: ‘Royal Dutch Shell announced figures that were overall below consensus forecasts, particularly at exploration and production levels.

Despite the results showing a rise in Q4 profit, investors should be aware that poor performance in the same period last year means the like-for-like rise is weaker than it appears.’

The oil giant, which employs 90,000 people in more than 70 countries, still made profits of £14.9billion overall for 2014, a rise of 16 per cent on a year earlier.

RELATED

The TRUTH will set you FREE.

From an article by Angela Macdonald-Smith published 30 Jan 2015 by The Sydney Morning Herald under the headline:

From an article by Angela Macdonald-Smith published 30 Jan 2015 by The Sydney Morning Herald under the headline:

By Puneet Kollipara

By Puneet Kollipara